Timekeeper Inc. manufactures clocks on a highly automated assembly line. Its costing system uses two cost categories, direct materials and conversion costs. Each product must pass through the Assembly Department and the Testing Department. Direct materials are added at the beginning of the production process. Conversion costs are allocated evenly throughout production. Timekeeper Inc. uses weighted-average costing.

Data for the Assembly Department for June 2017 are:

| Work in process, beginning inventory | 350 units |

Direct materials (100% complete)

Conversion costs (60% complete)

| Units started during June | 1030 units |

| Work in process, ending inventory: | 220 units |

Direct materials (100% complete)

Conversion costs (75% complete)

Costs for June 2017:

Work in process, beginning inventory:

| Direct materials costs added during June | $602,500 |

| Conversion costs added during June | $402,500 |

What is the direct materials cost per equivalent unit during June?

◦ $679.51

◦ $519.40

◦ $504.71

◦ $409.86

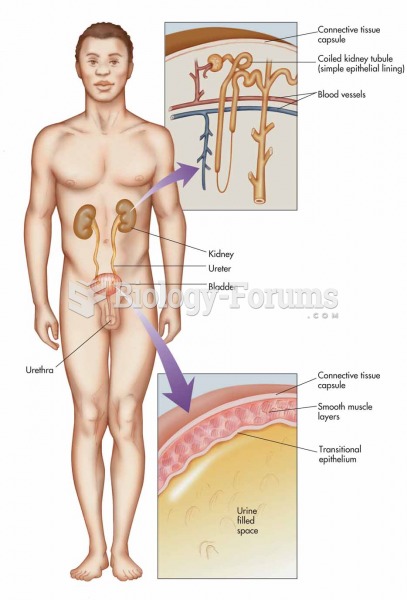

The urinary system: kidneys, ureters, bladder, and urethra with expanded view of a nephron and the u

The urinary system: kidneys, ureters, bladder, and urethra with expanded view of a nephron and the u

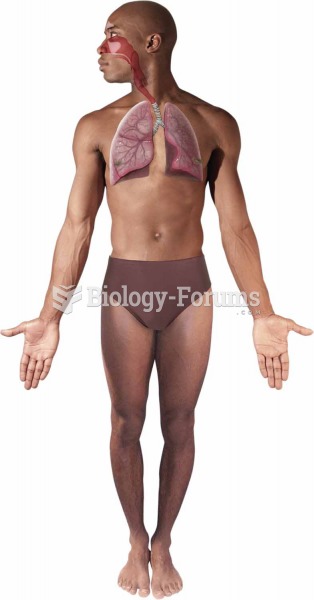

Respiratory system

Respiratory system

Integumentary system.Epidermis and dermis.

Integumentary system.Epidermis and dermis.

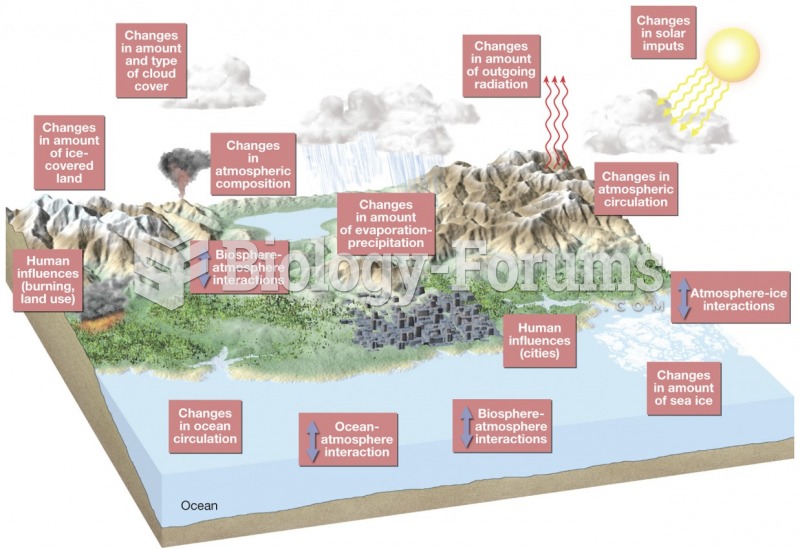

The Climate System

The Climate System

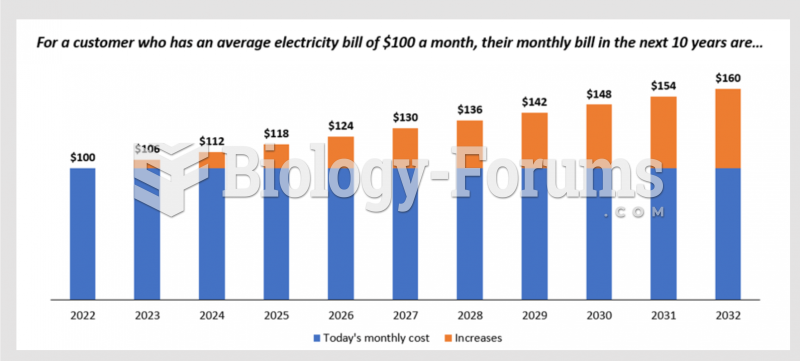

Ontario's electricity system four key components

Ontario's electricity system four key components

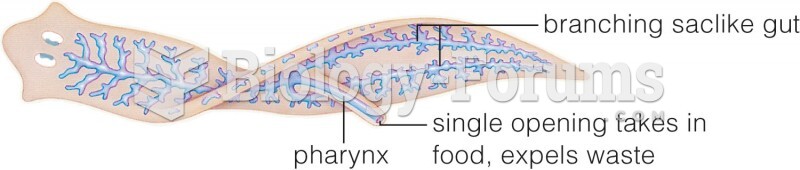

Incomplete Digestive System

Incomplete Digestive System