This topic contains a solution. Click here to go to the answer

|

|

|

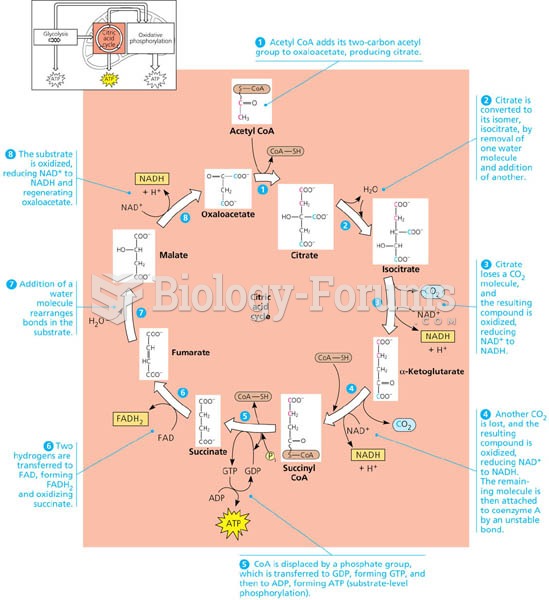

A closer look at the citric acid cycle

A closer look at the citric acid cycle

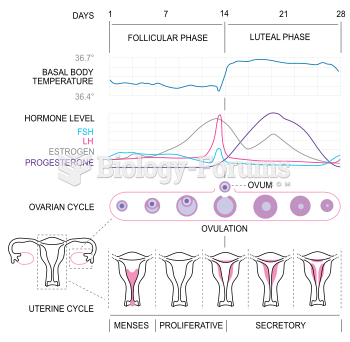

Menstrual Cycle

Menstrual Cycle

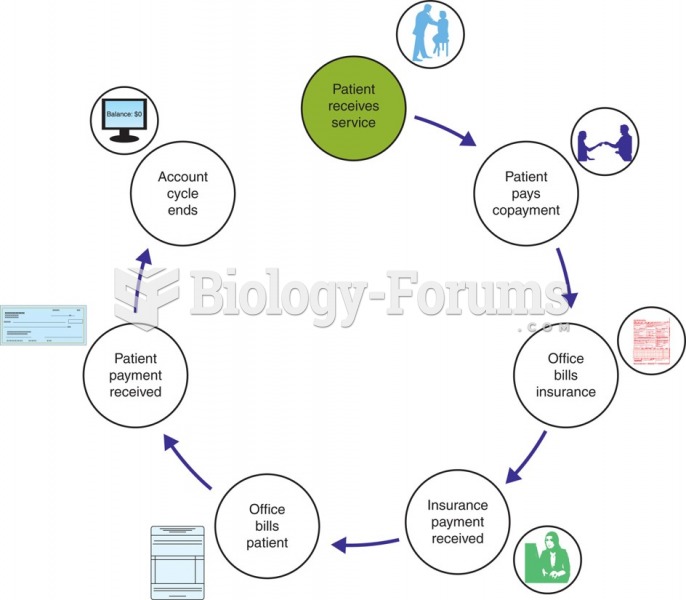

Accounts receivable cycle.

Accounts receivable cycle.

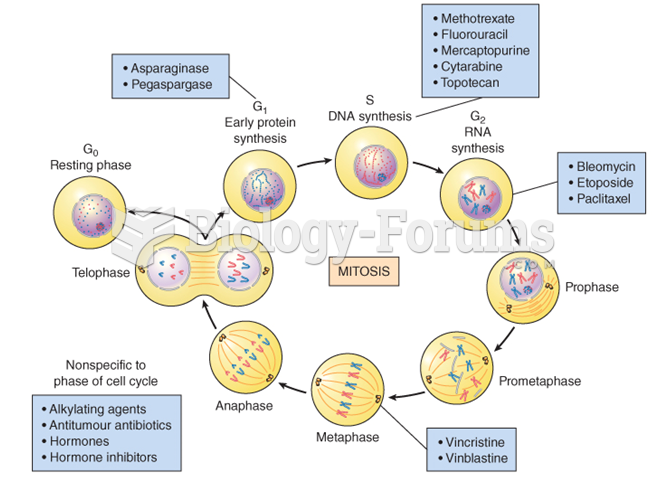

Antineoplastic drug and the cell cycle

Antineoplastic drug and the cell cycle

cell cycle

cell cycle

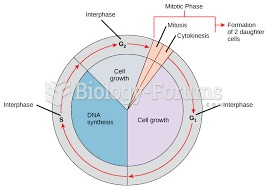

The normal cell cycle and each of its growth phases

The normal cell cycle and each of its growth phases