Total cost of production refers to the:

A) sum of variable costs and fixed costs.

B) product of variable costs and fixed costs.

C) difference between variable costs and fixed costs.

D) ratio of variable costs to fixed costs.

Question 2

When economists say that an interest rate is compounding, they imply that:

A) the rate of interest decreases every year.

B) the rate of interest increases every year.

C) interest is being earned on interest.

D) double the interest payment is received every two years.

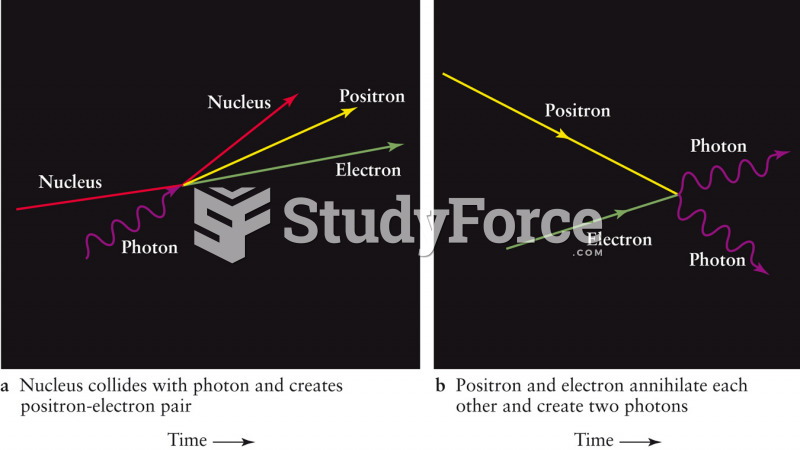

Pair Production and Annihilation

Pair Production and Annihilation

Increasing Costs of Natural Disasters

Increasing Costs of Natural Disasters

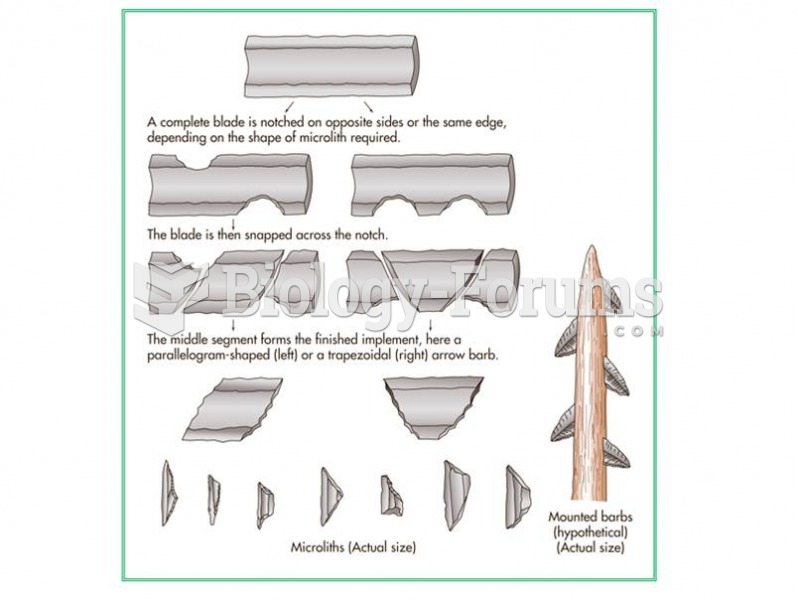

Microlith production.

Microlith production.

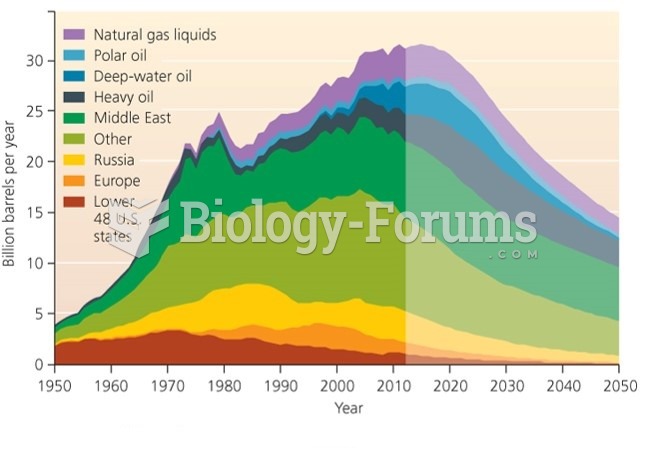

Modern Predication of Peak in Global Oil Production

Modern Predication of Peak in Global Oil Production

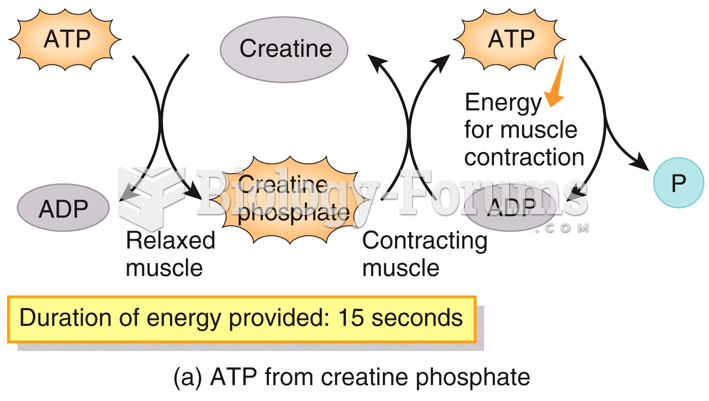

ATP Production in Cardiac Muscle

ATP Production in Cardiac Muscle

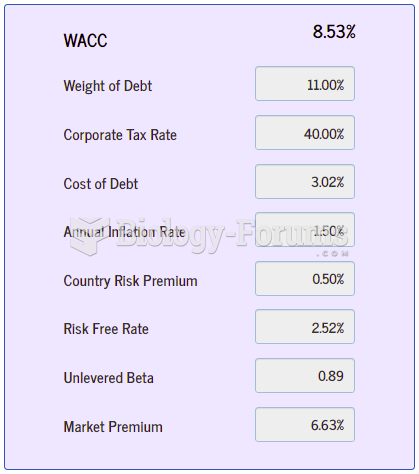

When operating your own business, it is wise to know your cost of capital and that of the ...

When operating your own business, it is wise to know your cost of capital and that of the ...