Total cost of production refers to the:

A) sum of variable costs and fixed costs.

B) product of variable costs and fixed costs.

C) difference between variable costs and fixed costs.

D) ratio of variable costs to fixed costs.

Question 2

When economists say that an interest rate is compounding, they imply that:

A) the rate of interest decreases every year.

B) the rate of interest increases every year.

C) interest is being earned on interest.

D) double the interest payment is received every two years.

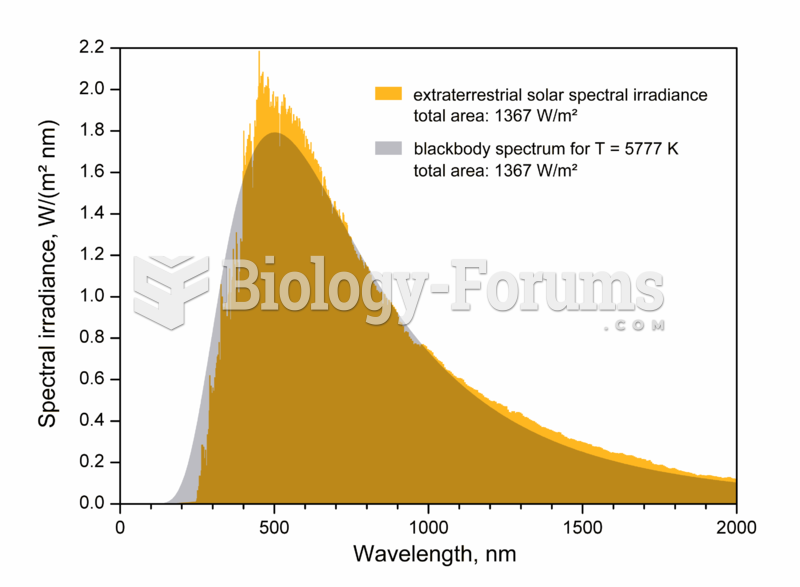

The effective temperature, or black body temperature, of the Sun (5777 K) is the temperature a black

The effective temperature, or black body temperature, of the Sun (5777 K) is the temperature a black

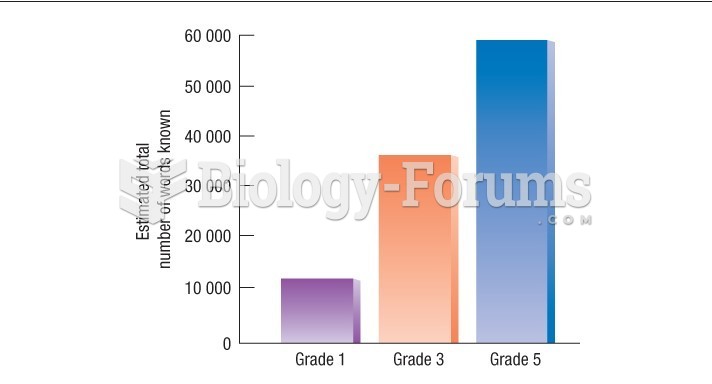

Anglin's estimates of the total vocabulary of children in Grades 1, 3, and 5

Anglin's estimates of the total vocabulary of children in Grades 1, 3, and 5

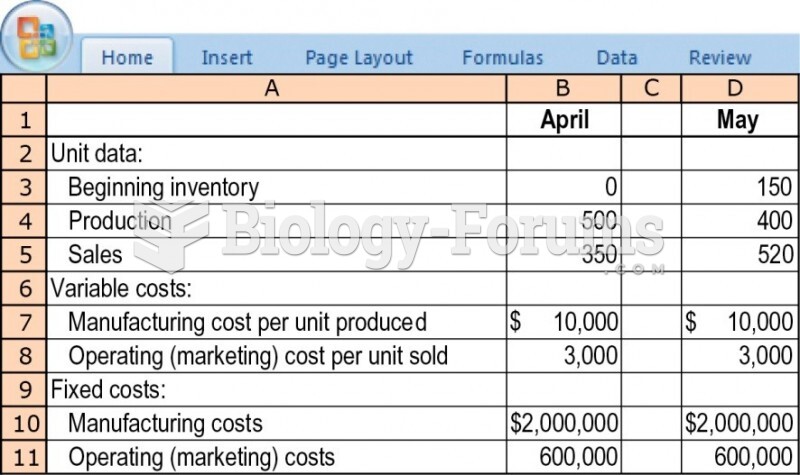

Variable and absorption costing, explaining operating-income differences.

Variable and absorption costing, explaining operating-income differences.

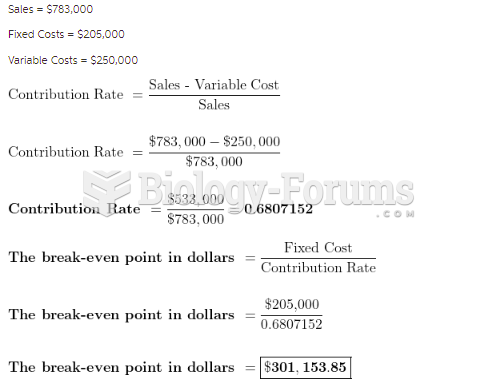

A company that makes environmental measuring devices has calculated their revenue and costs as ...

A company that makes environmental measuring devices has calculated their revenue and costs as ...

The production of a new allopolyploid species

The production of a new allopolyploid species

Production of colorless sectors and reversion of the unstable colorless

Production of colorless sectors and reversion of the unstable colorless