Answer to Question 1

b

Answer to Question 2

1. Because no beginning inventories exist, if PLF sells all 300,000 bulbs manufactured, its operating income will be the same under all four capacity options. Calculations are provided below:

Theoretical Practical Normal Master Budget

Revenue a 2,940,000 2,940,000 2,940,000 2,940,000

Less: Cost of goods sold b 1,110,000 1,395,000 2,070,000 2,280,000

Less: Production volume variance 780,000 U 495,000 U (180,000) F (390,000) F

Gross margin 1,050,000 1,050,000 1,050,000 1,050,000

Variable selling c 60,000 60,000 60,000 60,000

Fixed selling 220,000 220,000 220,000 220,000

Operating income 770,000 770,000 770,000 770,000

a300,000 9.80

b300,000 3.70, 4.65, 6.90, 7.60

c300,000 0.20

2. If the manager of PLF produces and sells 300,000 bulbs, then all capacity levels will result in the same operating income of 770,000 (see requirement 1 above). If the manager of PLF is able to sell only 225,000 of the bulbs produced and if the production-volume variance is closed to cost of goods sold, then the operating income is given as in requirement 3 of 9-36. Both sets of numbers are reproduced below.

Theoretical Practical Normal Master Budget

Income with sales of 300,000 bulbs 770,000 770,000 770,000 770,000

Income with sales of 225,000 bulbs 327,500 398,750 567,500 620,000

Decrease in income when

there is over-production 442,500 371,250 202,500 150,000

Comparing these results, it is clear that for a given level of overproduction relative to sales, the manager's performance will appear better if he/she uses as the denominator a level that is lower. In this example, setting the denominator to equal the master budget (the lowest of the four capacity levels here), minimizes the loss to the manager from being unable to sell the entire production quantity of 300,000 bulbs.

3. In this scenario, the manager of PLF produces 300,000 bulbs and sells 225,000 of them, and the production volume variance is prorated. Given the absence of ending work in process inventory or beginning inventory of any kind, the fraction of the production volume variance that is absorbed into the cost of goods sold is given by 225,000/300,000 or 75. The operating income under various denominator levels is then given by the following modification of the solution to requirement 3 of 9-36:

Theoretical Practical Normal Master Budget

Revenue 2,205,000 2,205,000 2,205,000 2,205,000

Less: Cost of goods sold 832,500 1,046,250 1,552,500 1,710,000

Less: Prorated production-volume variance a 585,000 U 371,250 U (135,000) F (292,500) F

Gross margin 787,500 787,500 787,500 787,500

Variable selling b 45,000 45,000 45,000 45,000

Fixed selling 220,000 220,000 220,000 220,000

Operating income 522,500 522,500 522,500 522,500

a (7/10) 665,000, 390,000, 140,000, (435,000)

b225,000 0.20

Under the proration approach, operating income is 522,500 regardless of the denominator initially used. Thus, in contrast to the case where the production volume variance is written off to cost of goods sold, there is no temptation under the proration approach for the manager to play games with the choice of denominator level.

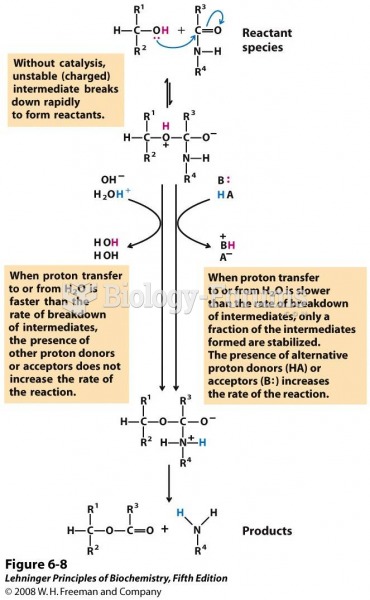

How a catalyst circumvents unfavorable charge development during cleavage of an amide

How a catalyst circumvents unfavorable charge development during cleavage of an amide

When the United States gets stuck over a controversial issue—usually something a divided Congress ca

When the United States gets stuck over a controversial issue—usually something a divided Congress ca

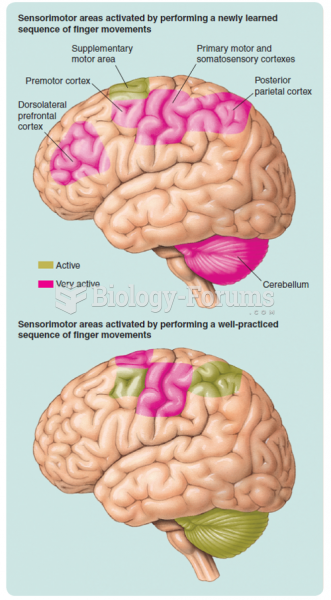

The activity recorded by PET scans during the performance of newly learned and well-practiced ...

The activity recorded by PET scans during the performance of newly learned and well-practiced ...

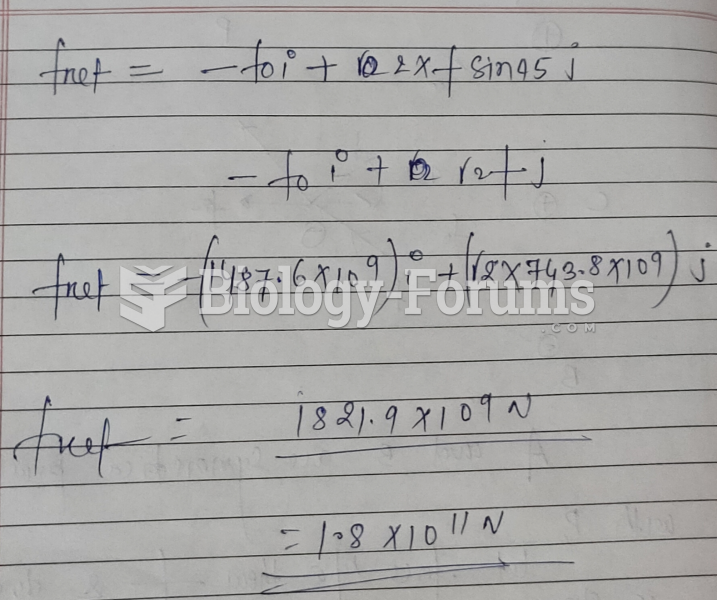

1) (a) What is Coulomb?s Law? (b) Find the net electrostatic force on the charge labeled ?P? in ...

1) (a) What is Coulomb?s Law? (b) Find the net electrostatic force on the charge labeled ?P? in ...

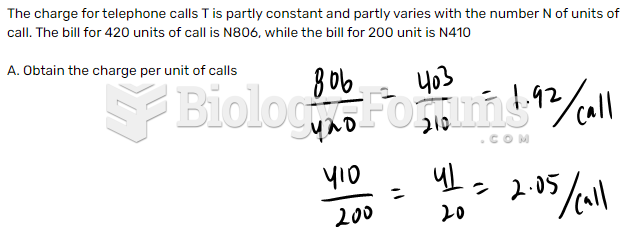

The charge for telephone calls T is partly constant and partly varies with the number N of ...

The charge for telephone calls T is partly constant and partly varies with the number N of ...

A promissory note for $600.OO dated January 15, 2017. requires an interest payment of $120 00 ...

A promissory note for $600.OO dated January 15, 2017. requires an interest payment of $120 00 ...