|

|

|

These species are all at risk of extinction. Species with slow life-h

These species are all at risk of extinction. Species with slow life-h

Free-roaming mustangs (Utah, 2005)

Free-roaming mustangs (Utah, 2005)

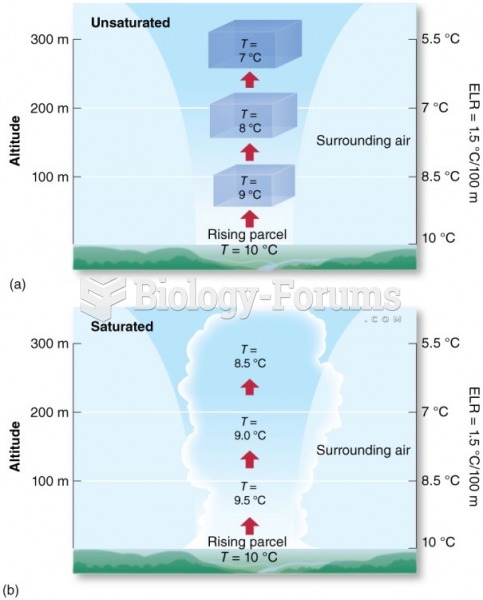

Static Stability & Environmental Lapse Rate

Static Stability & Environmental Lapse Rate

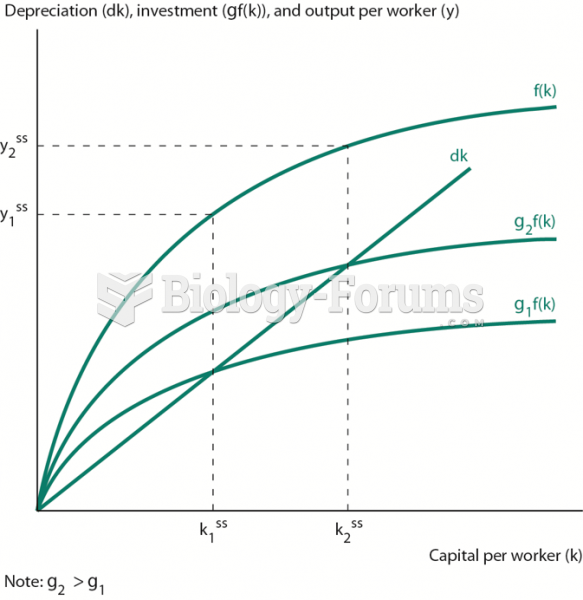

Effect of Increasing the Investment Rate on the Steady State

Effect of Increasing the Investment Rate on the Steady State

Stock Market Tracks Growth in GDP

Stock Market Tracks Growth in GDP

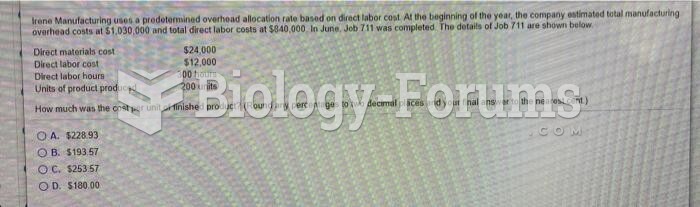

Irene Manufacturing uses a predetermined overhead allocation rate based on a percentage of ...

Irene Manufacturing uses a predetermined overhead allocation rate based on a percentage of ...