Answer to Question 1

Operating budgets are budgets that identify projected sales and production goals and the various costs a firm will incur to meet these goals. These budgets are developed in a specific order, with the information from earlier budgets used in the preparation of later budgets.

Financial budgets focus on a firm's financial goals and identify the resources needed to achieve these goals. The two main financial budget documents are the cash budget and the capital expenditure budget. The cash budget identifies short-term fluctuations in cash flows, helping managers identify times when the firm might face cash flow problems-or when it might have a temporary surplus of cash that it could invest. The capital expenditure budget identifies a firm's planned investments in major fixed assets and long-term projects. The information from these two financial budgets and the budgeted income statement are combined to construct the budgeted balance sheet. This is the last financial budget; it shows how the firm's operations, investing, and financing activities are expected to affect all of the asset, liability, and owners' equity accounts.

A firm's master budget organizes the operating and financial budgets into a unified whole, representing the firm's overall plan of action for a specified time period. In other words, the master budget shows how all of the pieces fit together to form a complete picture.

Answer to Question 2

B

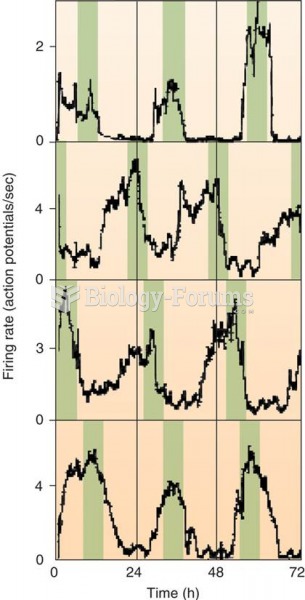

Firing Rate of Individual SCN Neurons in a Tissue Culture Color bars have been added to emphasize th

Firing Rate of Individual SCN Neurons in a Tissue Culture Color bars have been added to emphasize th

Question

Question

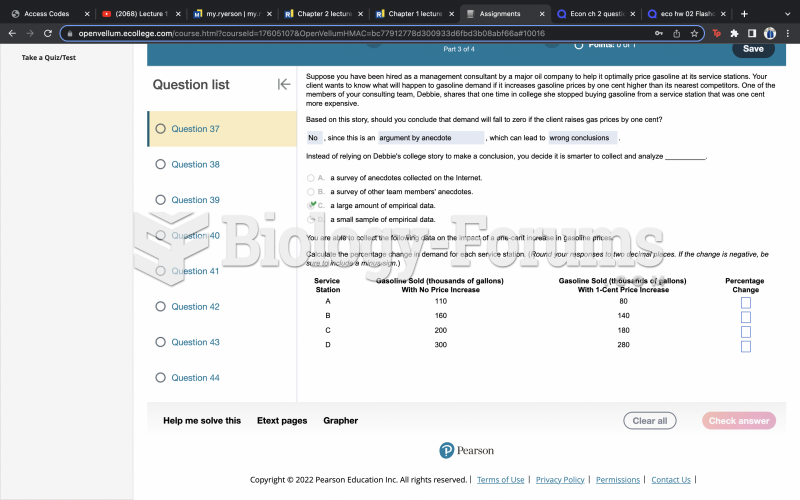

Question 37 Part 2

Question 37 Part 2

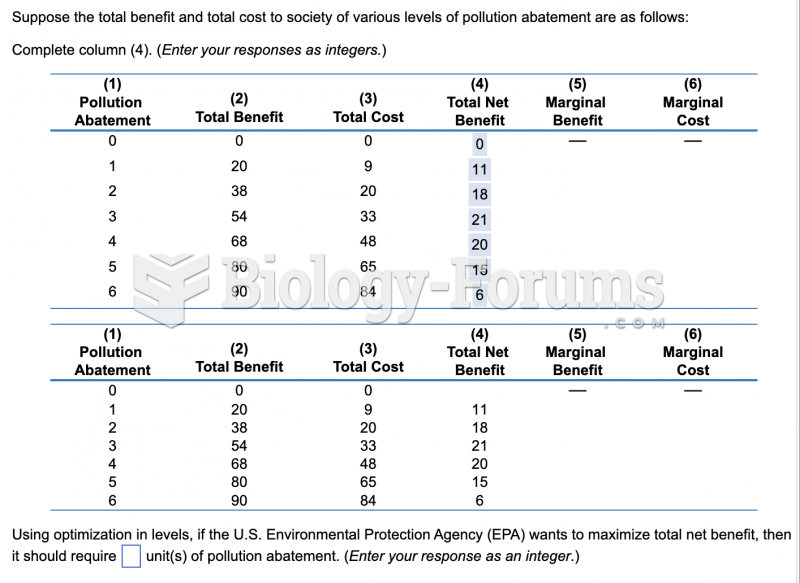

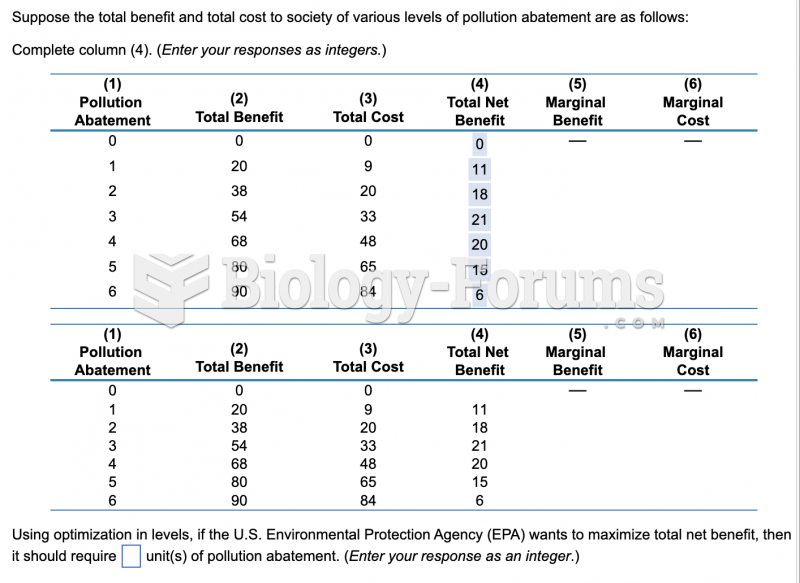

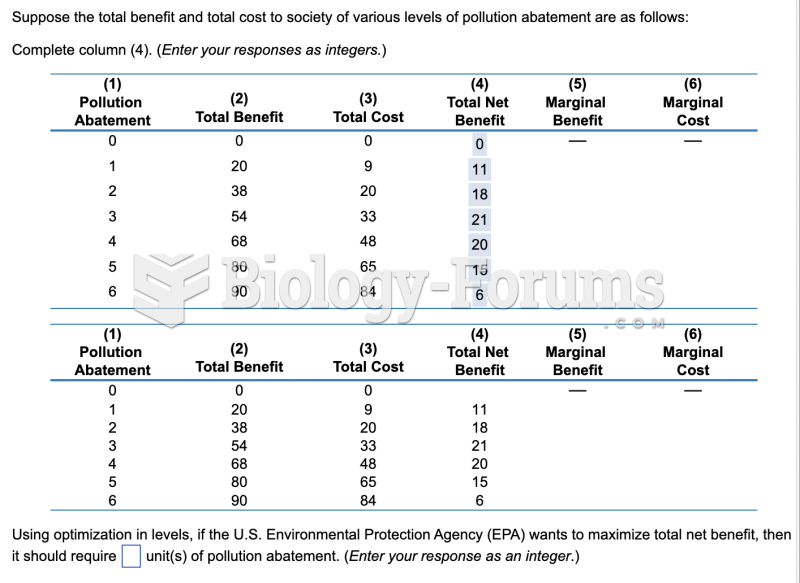

economic question

economic question

economic question

economic question

economic question

economic question