Answer to Question 1

A corporation is a business entity created by filing a form (known in most states as the articles of incorporation) with the appropriate state agency, paying the state's incorporation fees, and meeting other requirements. The specifics vary among states. Unlike a sole proprietorship or a partnership, a corporation is considered to be a legal entity that is separate and distinct from its owners. Because of a corporation's status as a separate legal entity, the owners of a corporation have limited liability-meaning they aren't personally responsible for the debts and obligations of their company.

A limited liability company (LLC) is a hybrid form of business ownership that is similar in some respects to a corporation while having other characteristics that are similar to a partnership. Like a corporation, a limited liability company is considered a legal entity separate from its owners. Also like a corporation-and as its name implies-an LLC offers its owners limited liability for the debts of their business. But it offers more flexibility than a corporation in terms of tax treatment; in fact, one of the most interesting characteristics of an LLC is that its owners can elect to have their business taxed either as a corporation or a partnership. Many states even allow individuals to form single-person LLCs that are taxed as if they were sole proprietorships.

Answer to Question 2

D

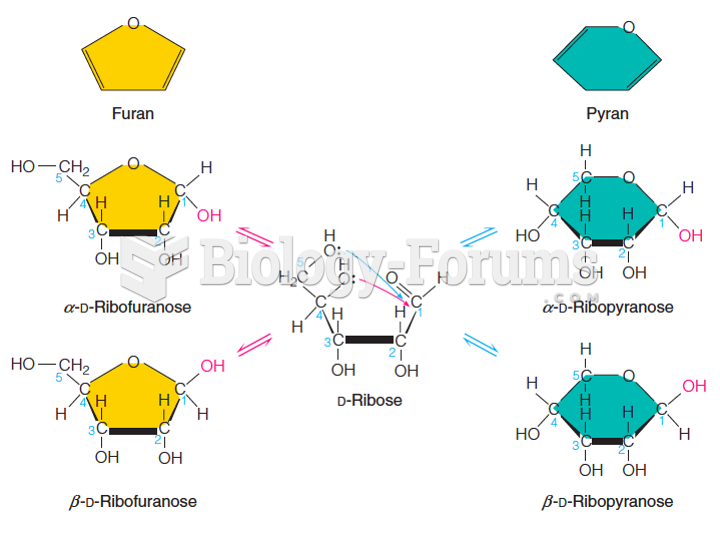

Two anomeric forms, and are possible, a and b.

Two anomeric forms, and are possible, a and b.

How to solve a trigonometric problem involving two right triangles (Question 2)

How to solve a trigonometric problem involving two right triangles (Question 2)

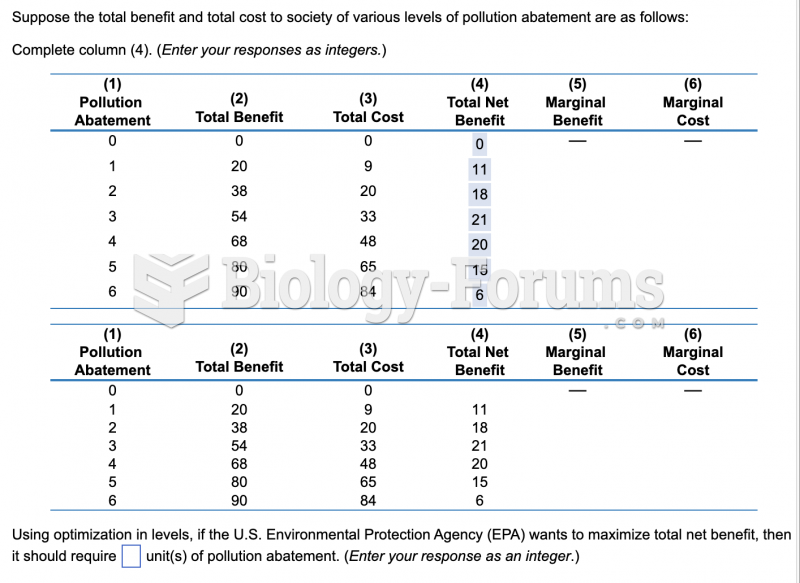

Economics question

Economics question

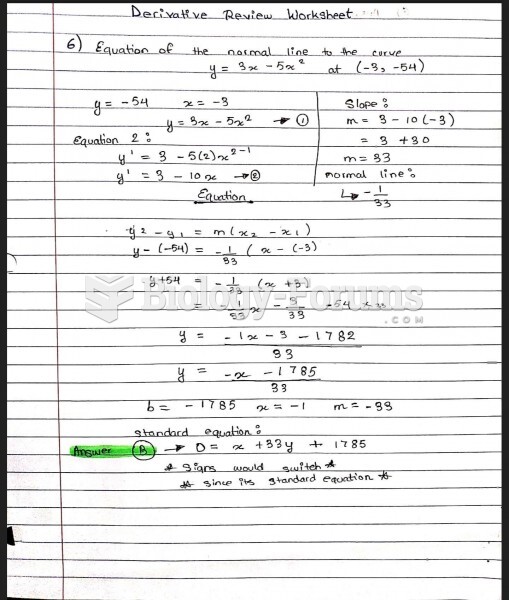

this is a math question

this is a math question

economic question

economic question

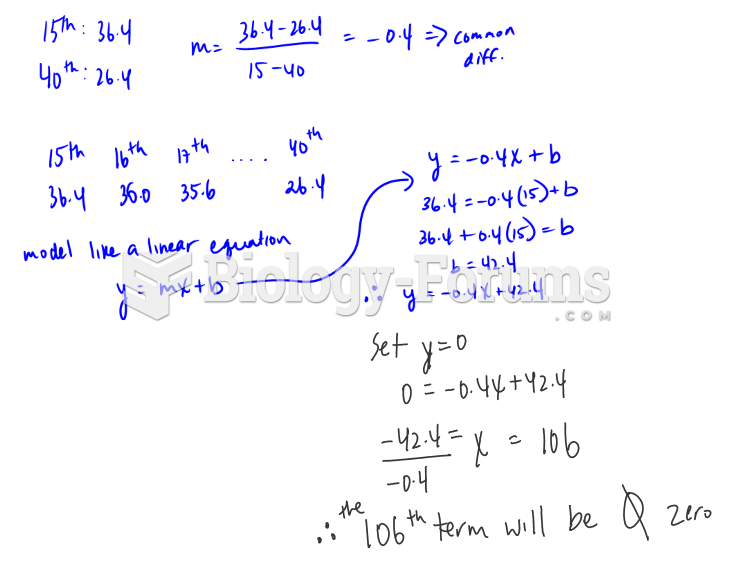

Mathematics Question

Mathematics Question