This topic contains a solution. Click here to go to the answer

|

|

|

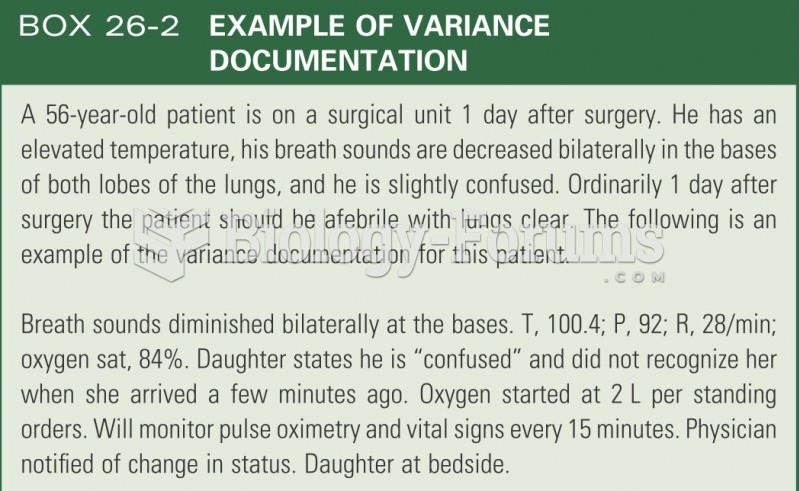

Example of variance documentation

Example of variance documentation

How to manually find the mean, variance, and standard deviation for a set of numbers

How to manually find the mean, variance, and standard deviation for a set of numbers

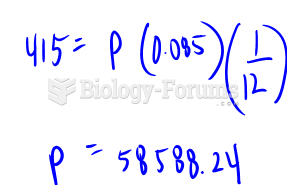

Philip wants to supplement his pension by $415 per month with income from his investments. His ...

Philip wants to supplement his pension by $415 per month with income from his investments. His ...

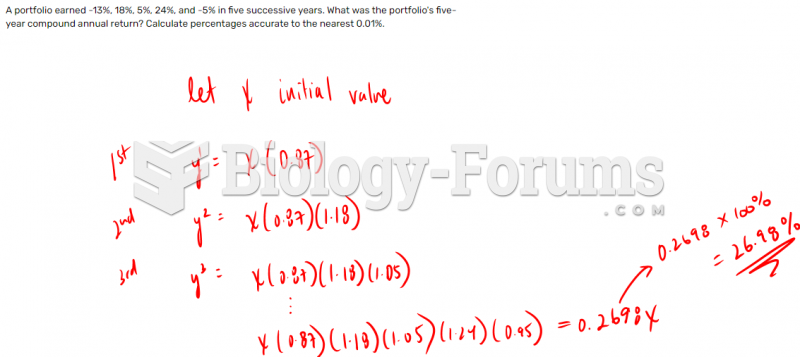

A portfolio earned -13%, 18%, 5%, 24%, and -5% in five successive years. What was the ...

A portfolio earned -13%, 18%, 5%, 24%, and -5% in five successive years. What was the ...

Distributions and variance

Distributions and variance

Sources of phenotypic variance

Sources of phenotypic variance